Article

D&O exposures: a dramatic evolution through 20 years of risk

Over the last two decades, the world of Directors & Officers (D&O) Liability has evolved dramatically.

As Beazley celebrates a combined 80 years of experience, we’re taking a moment to look back to 2005 and trace how the liability landscape has evolved and shifted across global markets.

Rewind back to 2005

Across the U.S., the UK, Europe and Asia-Pacific, D&O exposures were generally focused around financial risks. Litigation was largely built on shareholder losses due to financial misconduct, and regulatory scrutiny typically from financial authorities and led by the introduction of reforms like Sarbanes-Oxley (SOX) in the U.S., updates to the Combined Code on Corporate Governance in the UK and early corporate governance developments across Europe.

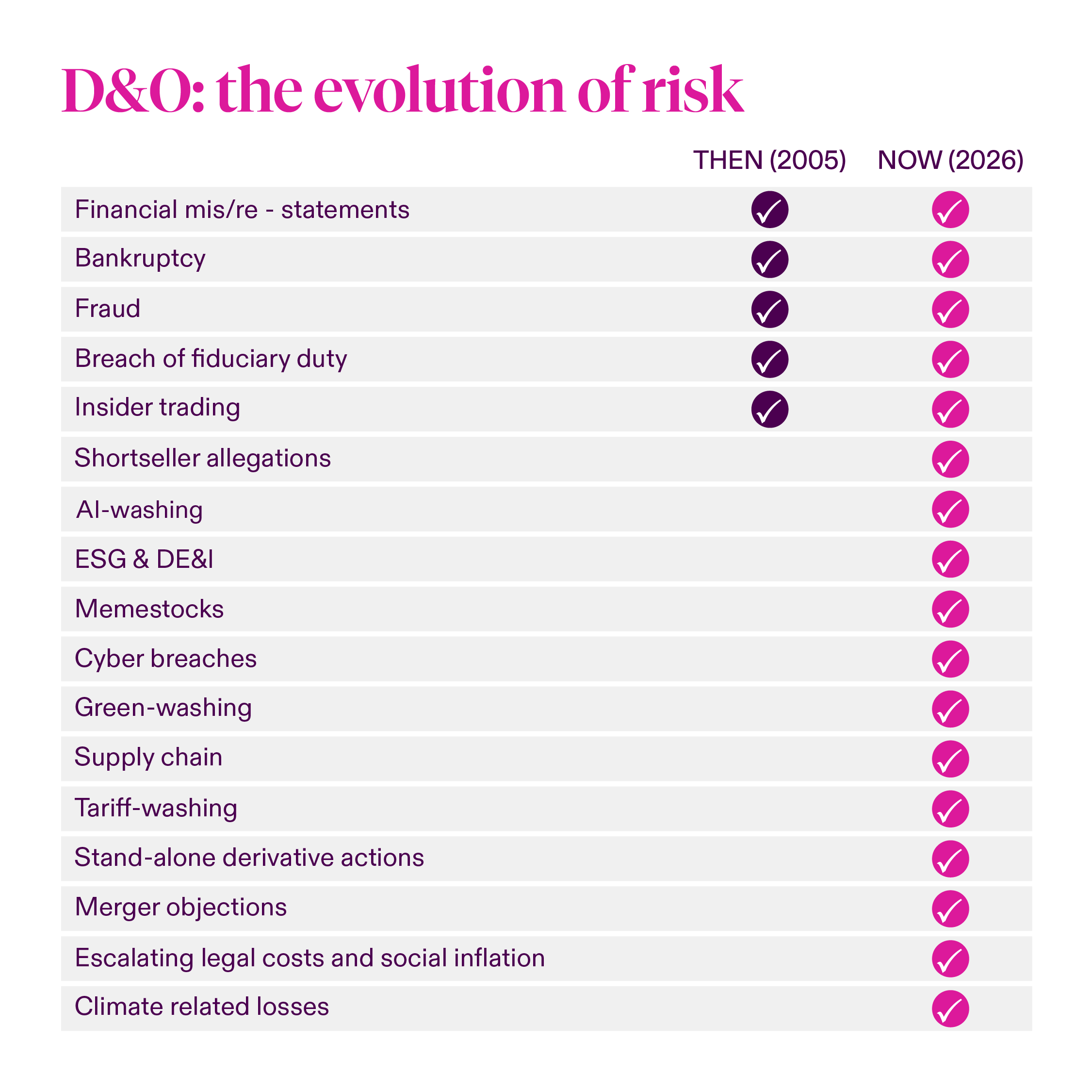

The scope of exposure was narrow and more predictable:

Financial Misstatements: Errors or manipulations in financial reporting i.e. erroneous financial reporting, restatement or allegations of false & misleading statements.

Bankruptcy: Claims arising from financial insolvency and mismanagement.

Fraud & Insider Trading: Synonymous with many of the scandals of the time included; the mis-use of corporate funds or information to enrich management at the detriment of shareholders. Classic securities violations.

Shareholder Class Actions: Primarily U.S.-centric, although derivative actions and regulatory investigations were increasing in Canada, Australia and parts of Europe as shareholder rights expanded.

D&O coverage was focused on Side A and Side B indemnification – Side C was emerging but still not widespread or consistent across regions.

And ESG and data breaches weren’t a part of the D&O vocabulary, once upon a time…

Fast forward

Things have changed! In 2026, the variety of D&O claims has expanded well beyond financial risks. Allegations may now stem from any action perceived as diminishing the organization's value. Directors and Officers face intensifying scrutiny from shareholders, shortsellers, regulators, the public, and activists. All of whom are empowered with the speed of the internet and the power of hindsight.

In addition to the risks outlined above, 2026 presents an increasingly dynamic environment with a broad range of exposures including, though not limited to:

Merger Objections: shareholders increasingly challenge M&A transactions, alleging undervaluation or conflicts of interest.

Legal Costs & Social Inflation: Rising litigation costs worldwide, record setting settlements for securities claims and derivative matters coupled with legal system abuse and broader jury awards, have made claims more expensive.

Cybersecurity: New regulatory regimes including GDPR in the EU have pushed cyber risk into the board room. A cyber-attack can lead to devastating reputational, financial, and shareholder concerns. It’s a core governance issue, which requires the appropriate investment of time, money and process from the executive team.

Memestocks: Volatile trading driven by social media hype, and not the fundamentals of the business, has led to lawsuits when boards are perceived as failing to manage or disclose risks adequately.

Shortseller Allegations: Activist short sellers can trigger stock drops and lawsuits especially if they lead to long drawn-out proxy battles or shareholder loss.

Supply Chain & Tariff Challenges: - Earnings challenges resultant from supply chain constraint, inflationary pressures or the impact of tariffs (both within the US and for companies that trade in the US) can impact on profitability leading to litigation.

AI, DEI or Greenwashing: Allegations of an organisational overstatement or under delivery of environmental goals and AI efficacy or the changes to a company’s DEI stance. In a heightened political landscape, a company’s decisions become even more scrutinized.

In Focus: Coverage Expansion

As exposures expand, so has coverage. The introduction of Side C coverage was only the beginning. Modern D&O policies now extend protection to a broader range of Insured Persons, including Chief Information Security Officers, Advisory Boards, and employed counsel. Enhanced Crisis Solutions have been added to base forms, and the inclusion of Entity Investigation coverage is a regular ask, though still subject to underwriting.

Even the policy language itself has modernized: simplified wordings, broader triggers, and enhanced protection for global exposures now reflect the market’s maturity.

Summary

Whether it’s financial mishandling or the latest -washing trend, D&O is a market that requires real knowhow, claims clout and long-term stability. Experience matters.

Experienced underwriting and claims expertise is a must, and our team ensures that organisations and their executives are resilient against the shifting sands of business liability landscape.

The information set forth in this communication is intended as general risk management information. Beazley does not render legal services or advice. Nothing in this communication should be construed or relied upon as legal advice or used as a substitute for consultation with counsel. Although reasonable care has been taken in preparing the information set forth in this communication, Beazley accepts no responsibility for any errors it may contain or for any losses allegedly attributable to this information